COURT RULES THAT “INSURED V. INSURED” EXCLUSION IN D&O POLICY BARS COVERAGE FOR INDEMNIFICATION OF CEO OF CORPORATION

May 12, 2016 in Case Law Updates by bronsteincarmona

In a decision issued by the First District Court of Appeal[1], the Court interpreted the “Insured v. Insured” exclusion of a Directors and Officers Liability Policy and precluded the ability of the Plaintiff to obtain indemnification from an insurance company.

Dennis Durant, a former director and shareholder of Bonifay Holding Co. Inc., sued the CEO of Bonifay in his individual capacity as a result of what was, in essence, a devaluation of Durant’s shares in the corporation. Durant obtained a judgment against the CEO and also sued Progressive Casualty Insurance Company alleging that the Director and Officer Liability policy issued to Bonifay covered the judgment against the CEO.

While Progressive had issued a policy of insurance covering monetary judgments against the directors and officers, the policy also included an “Insured v. Insured” exclusion. This exclusion stated that Progressive would not be obligated to pay judgments where the suit is brought by the insured person and arises out of the employment of the insured person. Because Durant was admittedly a former director of Bonifay Holdings, and the policy defined “insured persons” as “any past, present or future director, trustee, officer, employee […] of the Company […]”, the Court reasoned that Durant qualified as an insured party under the policy.

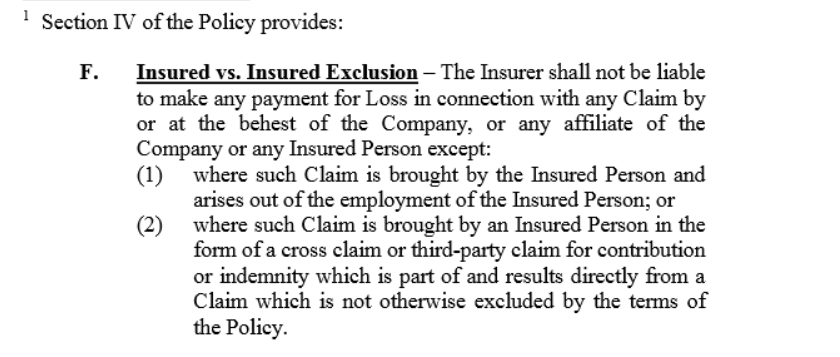

Progressive’s “Insured v. Insured” exclusion read as follows:

The Court further disagreed with Durant’s argument that the exclusion did not apply in his case because he was suing as an individual, not in his capacity of a director or officer. Durant’s also argued that Florida Statute 607.01401(10) created an “exception” (coverage despite the exclusion) because the claim arose out of Durant’s employment with Bonifay and the statute provides that a corporate director is not an employee of the company, but that he or she “may accept duties that make him or her also an employee”. The Court denied Durant’s argument because that there was no evidence presented at the trial level showing that Durant accepted any duties beyond those required of a director

Durant’s case demonstrates that “Insured v. Insured” exclusions must be reviewed carefully to determine whether coverage should or should not be extended and whether suit should be brought against the insurer. These types of legal assessments will be based almost entirely on the language of the particular policies and the factual situations that give rise to the controversy.

[1] Dennis Durant v. Brian James and Progressive Casualty Insurance Company, 41 Fla.L.Weekly D838 (Fla. 1st DCA April 4, 2016)